The Thailand

Finance

Playbook

Your Financial Edge in Thailand

Every year, thousands of expats and nomads lose hundreds of dollars to Thailand's hidden financial traps — the 220 THB ATM fee, Dynamic Currency Conversion, tourist SIM markups, and the near-impossible task of opening a bank account on a DTV visa. This guide doesn't just identify the problems. It gives you the data, the numbers, and the playbook to beat every single one of them.

From getting 1,000 Baht in your hand at the cheapest possible cost, to investing in the Thai stock market and buying property as a foreigner — this is the financial operating manual that nobody at the airport bothered to hand you.

Table of Contents

-

1 Money & Payments: Stop Overpaying

- The 1,000 Baht Trap: A $10 Mistake on a $30 Transaction

- The 7 Payment Scenarios Ranked by Cost

- The ATM Fee & DCC Trap Explained

- Scan to Pay: TrueMoney & PromptPay Guide

- The SIM Card Tourist Tax & The Mall Hack

-

2 Banking in Thailand

- Why Opening a Thai Bank Account is So Hard in 2026

- Which Banks Accept DTV Visa Holders?

- Path 1: The DIY Method & The PA Insurance Trick

- Path 2: The Institutional Guarantor Method

- Your Financial Plan B: Fintech Tools

-

3 Investing in Thailand

- The Bull Case vs. The Bear Case

- The Stock Market (SET): Indices, ETFs & Blue Chips

- Property Investment: Legal Structures for Foreigners

- Freehold Condos, Leasehold & Thai Company Structures

- The 10-Year LTR Visa: The Property Investor's Advantage

-

4 Retiring in Thailand

- 2026 Cost of Living by City: Bangkok, Chiang Mai, Pattaya

- Debunking the "Early Retirement" Myth

- Visa & Financial Requirements for Retirees

- The 2026 Tax Reality: What You Actually Owe

- Savings Runway: How Long Will Your Money Last?

- A Appendix: Trusted Resources & Official Links

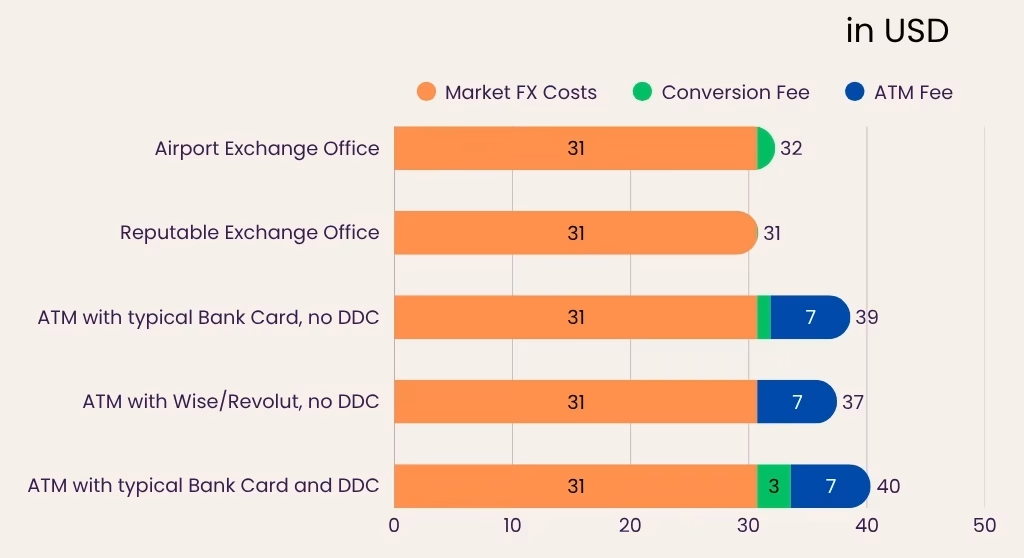

The 1,000 Baht Trap

To illustrate how much your payment choices matter, we ran a definitive experiment: how much does it really cost in US Dollars to either get 1,000 THB in cash or pay for a 1,000 THB item? The difference between the best and worst method is nearly $10 for the exact same value. The following rates were used as the basis for calculation (2025 average):

Part 1: Getting 1,000 THB in Cash

| # | Scenario | Method | Final Cost (USD) |

|---|---|---|---|

| Bar 1 | The Unprepared Tourist | Airport Exchange Counter at ~31.00 THB/USD | $32.26 |

| Bar 2 | The Savvy Cash Exchanger | City Exchange (SuperRich) at 32.44 THB/USD | $30.83 |

| Bar 3 | The Standard ATM User | ATM Withdrawal + 220 THB fee + 3% foreign transaction fee | $38.61 |

| Bar 4 | The Modern Traveler (Wise/Revolut) | ATM Withdrawal at mid-market rate + 220 THB ATM fee | $37.49 |

| Bar 5 | The Worst-Case ATM User | ATM with Dynamic Currency Conversion (DCC) accepted | $40.32 |

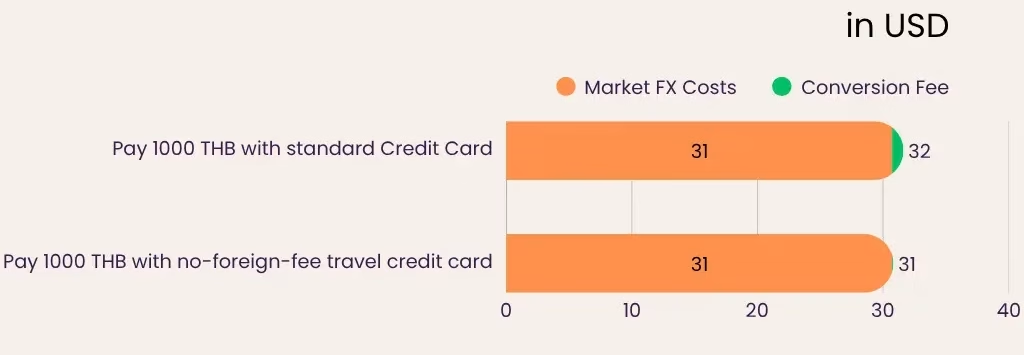

Part 2: Paying by Card for a 1,000 THB Item

| # | Scenario | Method | Final Cost (USD) |

|---|---|---|---|

| Bar 6 | The Standard Card User | Credit card with 3% foreign transaction fee | $31.65 |

| Bar 7 | The Smart Card User | Wise, Revolut, or no-foreign-fee card — mid-market rate, zero fees | $30.73 |

The Three Traps Behind the Numbers

Your Optimal Financial Strategy

- Pay by card whenever possible using a zero-fee card (Wise, Revolut) — the undisputed cheapest option at $30.73 per 1,000 THB.

- For cash, exchange at a reputable city booth like SuperRich in Bangkok. Never exchange at the airport.

- Use ATMs only for large withdrawals (10,000 THB+) to spread the flat 220 THB fee over a bigger sum. Always decline DCC.

🏦 The Best Cards for Thailand in 2026

- Wise: Mid-market exchange rate, low fees on currency exchange, free ATM withdrawals up to a monthly limit. You can open a Wise account from Thailand, but get the physical card delivered at home before you leave.

- Revolut: Similar benefits to Wise, with excellent app controls. Critical: You generally cannot open a Revolut account with a Thai address. Open and receive the card at home first.

- No-Fee Travel Credit Cards: Cards like Charles Schwab (US) or similar from your home country that refund ATM fees globally are also excellent tools.

Scan to Pay: TrueMoney & PromptPay

Thailand runs on QR codes. The PromptPay network is now integrated with Singapore (PayNow), Malaysia (DuitNow), and others across ASEAN. For tourists and DTV holders without a Thai bank account, the answer is the TrueMoney Wallet — Thailand's equivalent of Alipay.

Quick Guide: TrueMoney for Foreigners

| Platform | PromptPay Compatible | Foreigner Access | Best Use |

|---|---|---|---|

| TrueMoney Wallet | 100% (if fully verified) | High — passport + secondary ID often needed | Primary tool. Zero transaction fees. |

| Moreta Pay | 100% — built for tourists | Very High — no Thai ID required | Best fallback. Higher fees but guaranteed access. |

| Rabbit LINE Pay | Limited | Moderate — card linkage required | Secondary / transport use. |

💡 The TrueMoney WeCard Trick

Inside TrueMoney, enable the "TrueMoney WeCard" — a virtual Mastercard number. Many Thai websites (Lion Air, Major Cineplex, Lazada Thailand) reject foreign credit cards but accept this card as "Thai-issued." Users report saving up to 70% on airline baggage fees by paying online via WeCard rather than at the airport counter.The SIM Card Tourist Tax & The Mall Hack

The moment you land at Suvarnabhumi, you'll see neon signs: "Unlimited 5G Tourist SIM: 1,199 THB." This is a 240% tourist tax levied on your first hour of ignorance. The exact same service — indistinguishable in daily use — is available from official shops for around 350 THB total.

| Feature | Tourist SIM ("Farang" Tax) | Local SIM (The One SIM) |

|---|---|---|

| Upfront Cost | 699 – 1,199 THB | ~50 THB |

| 30-Day Data Add-On | Bundled at high price | ~300 THB via promo code at official store |

| Total Cost | ~1,200 THB | ~350 THB |

| Speed Difference | Unthrottled 5G (300 Mbps+) | Capped at 20–30 Mbps (sufficient for Zoom and 1080p) |

| Where to Buy | Airport kiosks, tourist zones | Official mall shops only (AIS Shop, True Shop) |

📍 The Mall Hack: Step-by-Step (Save 70%)

- Skip the airport kiosk entirely. Connect to airport WiFi and use it to order a Grab or Bolt.

- Head to a major mall — Central Festival, Terminal 21, CentralWorld, or MAYA. Find the official AIS Shop or Telewiz/True Shop (not 7-Eleven).

- Ask for "The One SIM" or a "Standard Prepaid SIM" (~50 THB). Corporate stores have full inventory and biometric equipment for instant passport registration.

- Ask staff to activate the "30-day Net 300 Baht" promo immediately. They have dealer codes to apply it on the spot.

- Before leaving the counter: Download the carrier app and complete login (requires an OTP to your new number). This ensures you can top up digitally later.

Total cost: ~350 THB ($10). Savings vs. airport: ~$25.

AIS or True — Which to Choose?

Since the True-dtac merger, prices are identical. Choose AIS for remote islands and mountain coverage (Koh Tao, Koh Lipe, Chiang Rai highlands). Choose True for superior 5G density in Bangkok, Pattaya, and Phuket city centers. For expats managing overseas bank OTPs: keep your home SIM in Slot 2, disable data roaming, and enable WiFi Calling before you leave your country. You'll receive SMS OTPs over the Thai data connection for free.

Why This Is So Hard in 2026

If you are struggling to open a Thai bank account on a DTV visa, it is not you — it is the system. Since 2024, Thai banks have severely tightened their policies under government pressure to combat "mule accounts" used by criminal syndicates to launder money from online gambling and romance scams. There have been serious cases of bank employees helping criminals forge documents, resulting in a mandate for far stricter internal controls.

The critical issue: despite its 5-year validity, banks officially classify the DTV as a special tourist visa. Under the new rules, tourist-category visas are explicitly ineligible for new bank accounts. Walk-in applications without an institutional guarantor now have a 90% rejection rate.

Which Banks Accept DTV Holders?

| Bank | DTV Policy (2026) | Key Notes |

|---|---|---|

| Bangkok Bank | Most Friendly | Often requires purchasing PA Insurance (~5,900 THB/year) as a condition for approval. Best success at the Silom Head Office. Best overall option for DIY attempts. |

| SCB (Siam Commercial) | Mixed | Requires a specific "Letter of Guarantee" from a government body or high-tier educational institution. Success varies by branch. |

| Kasikornbank (KBank) | Difficult | Generally classifies DTV as "Tourist" and rejects without a Work Permit, unless introduced via a "Soft Power" partner institution. |

| Krungsri (BAY) | Strict | Enforces "Work Permit only" policies in most branches. Not recommended for DTV holders without a guarantor. |

The Two Paths to Opening an Account

| Feature | Path 1: DIY Method | Path 2: Institutional Guarantor |

|---|---|---|

| Likelihood of Success | Very Low. Success depends entirely on finding a lenient branch manager willing to override official policy. | High. The bank trusts an accredited school to vet the applicant. This is the most reliable method in 2026. |

| Key Requirement | Certificate of Residence (COR) from Thai Immigration — the bare minimum. Without it, your chances are near zero. | Proof of enrollment in a long-term accredited course (Muay Thai, Thai cooking) with a school that has a formal bank partnership. |

| Primary Challenge | Finding a branch that says yes. Expect multiple rejections. | Finding an eligible school that offers this service. Confirm nationality restrictions upfront — some schools exclude certain nationalities. |

| Cost | Standard bank fees only (if successful). May require PA Insurance at Bangkok Bank (~5,900 THB). | Service fee to the institution (~5,000 THB) plus any standard bank fees. |

Path 1: DIY — Minimum Required Documents

- Passport with valid DTV visa stamp

- Certificate of Residence (COR) — obtained from the Thai Immigration Bureau. This is non-negotiable and the single most powerful document you can bring.

- Long-term lease agreement in your name (6 or 12 months). Most banks in 2026 require you to take this to Immigration first to get a formal COR — the lease alone is no longer sufficient.

- Supporting evidence: Home bank reference letter, proof of funds (the 500,000 THB required for the DTV), and your home country Tax Identification Number (TIN).

- Minimum deposit: 500–2,000 THB cash

The "PA Insurance" Lever at Bangkok Bank

If you attempt the DIY route at Bangkok Bank, be prepared to purchase Personal Accident (PA) Insurance. While officially "voluntary," branch staff in 2026 frequently make account opening conditional on purchasing a policy costing 3,000–6,000 THB. Many DTV holders report immediate approval once they agree to this. Factor it into your budget if Bangkok Bank is your target.Path 2: The Institutional Guarantor — What to Expect

The most successful path for DTV holders on "Soft Power" activities. A large, accredited Muay Thai gym or professional cooking school that has a formal bank partnership will act as your guarantor. Here is what a legitimate guarantor service involves:

- The school prepares a full dossier for the bank: accreditation from the Ministry of Education, business registration, licenses, and proof of financial stability (banks may look for annual revenues of 30 million THB or more to consider the school a trustworthy partner).

- A school staff member schedules the appointment and physically accompanies you to a pre-arranged branch. This personal escort is the signal to the bank that you are part of a trusted partnership.

- Expect a service fee of around 5,000 THB, separate from any bank charges.

- Nationality restrictions may apply. Common exclusions include nationals from Russia, India, Pakistan, China, and Nigeria, among others. Confirm before paying for a course or service.

Plan B: Managing Finances Without a Thai Account

Because opening an account can take weeks or months, you must have a robust financial plan for daily life in the interim. Relying on your home bank card and cash ATM withdrawals is expensive and unreliable.

| Service | Best For | Critical Caveat |

|---|---|---|

| Revolut | Daily spending with a physical card at mid-market rates. No foreign transaction fees. The best tool for everyday life in Thailand. | Must open the account and receive the physical card in your home country BEFORE arriving in Thailand. You cannot apply with a Thai address. |

| Wise | Sending larger sums of money from your home country to a Thai bank account at low cost and excellent exchange rates. | The physical Wise debit card is generally not deliverable to Thailand. Its primary function for DTV holders is as a transfer service, not for daily card spending. |

✅ Pre-Departure Banking Checklist

The Bull vs. Bear Case

Thailand presents a fascinating paradox for foreign investors: Southeast Asia's second-largest economy with a well-developed infrastructure, yet a stock market that has delivered nearly zero capital growth in THB over the past decade. Understanding this disconnect is the foundation of any intelligent investment decision here.

The Bull Case at a Glance

- Record Investment Pledges: Foreign investment commitments hit an 11-year high in 2025 — 42 billion USD as of Q3 2025 — led by digital (Google, Microsoft data centers) and EV sectors.

- Strategic Trade Deals: Thailand and the EFTA states (including Switzerland) signed a landmark Free Trade Agreement in January 2025, promising reduced barriers for European investors (pending ratification ~2027).

- BOI Incentives: The Board of Investment offers up to 8-year corporate tax exemptions and 100% foreign ownership rights for promoted companies in key sectors (EV, semiconductors, digital).

- The "Ignite Thailand" Vision: Eight priority growth sectors targeted by government, creating long-term structural tailwinds if execution follows.

- Slowing GDP: Growth estimated at 2.1% in 2025, falling to 1.5% in 2026 — significantly below the regional average. Household debt stands at 88.4% of GDP.

- Poor Market Returns: The SET index fell approximately 7.2% in 2025, following years of flat or negative price returns. The S&P 500 has more than tripled since 2016; the SET has lost value in the same period.

- US Tariff Headwind: A 19% reciprocal tariff on Thai goods (effective August 2025) adds a costly layer for Thai exporters, compounding pressure on an already weakened market.

- Currency Overvaluation Risk: The Baht is at a multi-year high of ~31.24 THB/USD as of January 2026. While this has benefited USD investors historically, it is now hurting tourism (making Thailand expensive for Chinese visitors) and export competitiveness. A future reversion could wipe out stock market gains.

- Chinese Tourism Decline: A notable drop in Chinese arrivals in early 2025 has hurt two of Thailand's most critical economic pillars simultaneously.

The Stock Market (SET)

For most foreign investors, the simplest entry point is through an ETF or the broad SET index. The data tells a clear story: essentially all local-currency returns for long-term investors have come from dividends, not capital appreciation.

The hidden saving grace for USD-based investors: the Baht strengthened from ~35.3 THB/USD in 2016 to ~31.2 THB/USD in 2026 — a 13% currency gain on top of dividend returns. Even a 0% THB return became a 13% USD return simply from currency movement. A future weakening of the Baht (likely, given current overvaluation) could reverse this entirely for new investors entering today.

Blue-Chip Performance Snapshot

| Stock | Sector | 5-Year Return (Approx.) | The Investment Thesis |

|---|---|---|---|

| BDMS (Bangkok Dusit Medical) | Healthcare / Medical Tourism | +3% | Stability over growth. Preserved capital during the pandemic. A bet on aging populations and medical tourism, not high growth. |

| AOT (Airports of Thailand) | Transport / Tourism | -33% | High-risk contrarian bet on full Chinese tourism recovery. Severely punished by the pandemic and slow to recover. |

| CPALL (7-Eleven Thailand) | Consumer Staples | -29% | Once defensive, now a value bet. High household debt has squeezed consumer spending, eliminating its defensive properties. |

How to Invest from Abroad

- International ETF (Simplest): Buy the iShares MSCI Thailand ETF (NYSE: THD) via any major international broker. No Thai account needed.

- Direct SET Access: Interactive Brokers (IBKR) is the gold standard for non-US expats — accepts residents from 200+ countries, multi-currency accounts including THB, and direct SET market access. Saxo Bank is the premium European alternative. Swissquote offers Swiss-bank security for European investors.

- Tax Note: Capital gains from Thai stocks are tax-exempt for individuals. Dividends are subject to a 10% withholding tax at source.

Property Investment for Foreigners

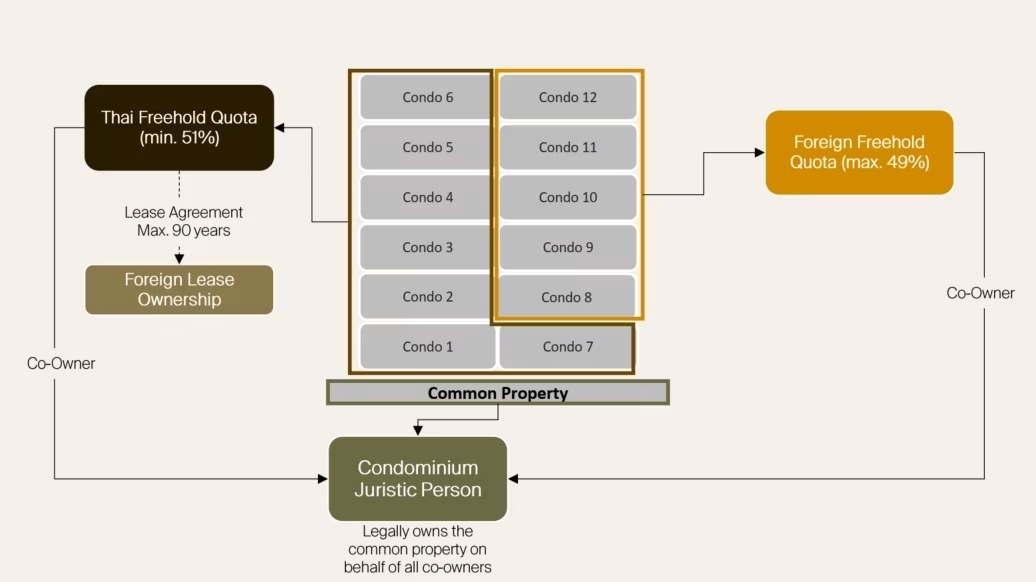

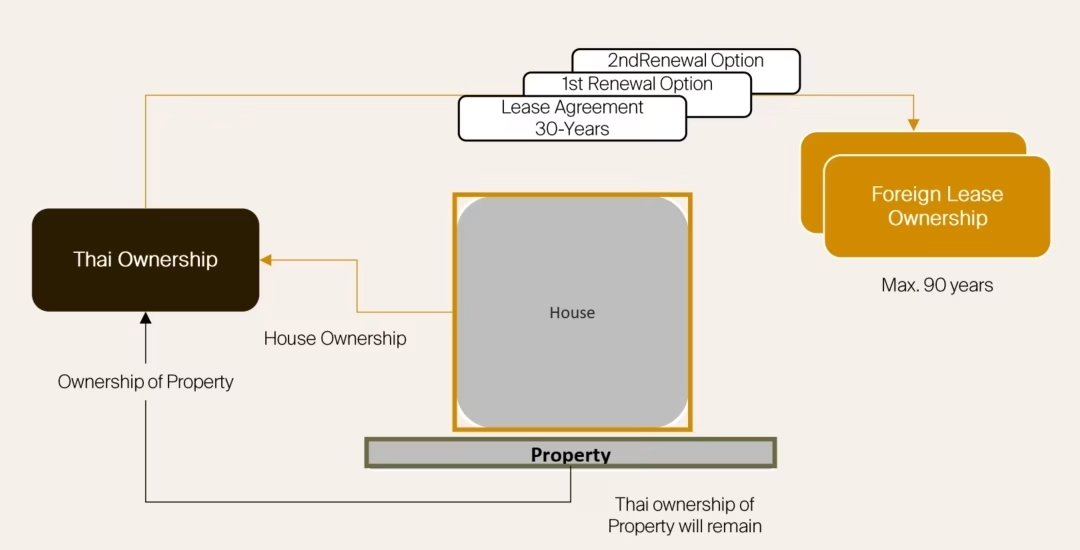

The cornerstone of Thai property law for foreigners: you cannot own land outright. The Condominium Act permits foreigners to own condo units in their own name, provided the building's foreign ownership does not exceed 49% of total saleable area. For anything involving land — houses, villas, plots — more complex legal structures are required.

| Ownership Type | What You Can Own | Risk Level | Best For |

|---|---|---|---|

| Freehold Condo | Condo unit outright, full title deed in your name. Max 49% of building. | Low | Most foreigners. Simplest and safest structure. |

| Leasehold (Land/House) | 30-year registered lease + renewal options (up to 90 years). You own the structure, not the land. | Medium | Those wanting a villa or house. Requires careful lawyer-drafted contract. |

| Thai Company (Holding) | Company owns the land; you control the company as Managing Director with 49% ordinary (voting) shares. | Medium–High | Sophisticated investors. Company must be a real operating business, not a shell. |

| Nominee Company | Shell company with Thai "nominees" holding 51% on paper. | Very High | Do not use in 2026. Government technology now actively identifies these. Asset seizure risk is real. |

The Leasehold Structure

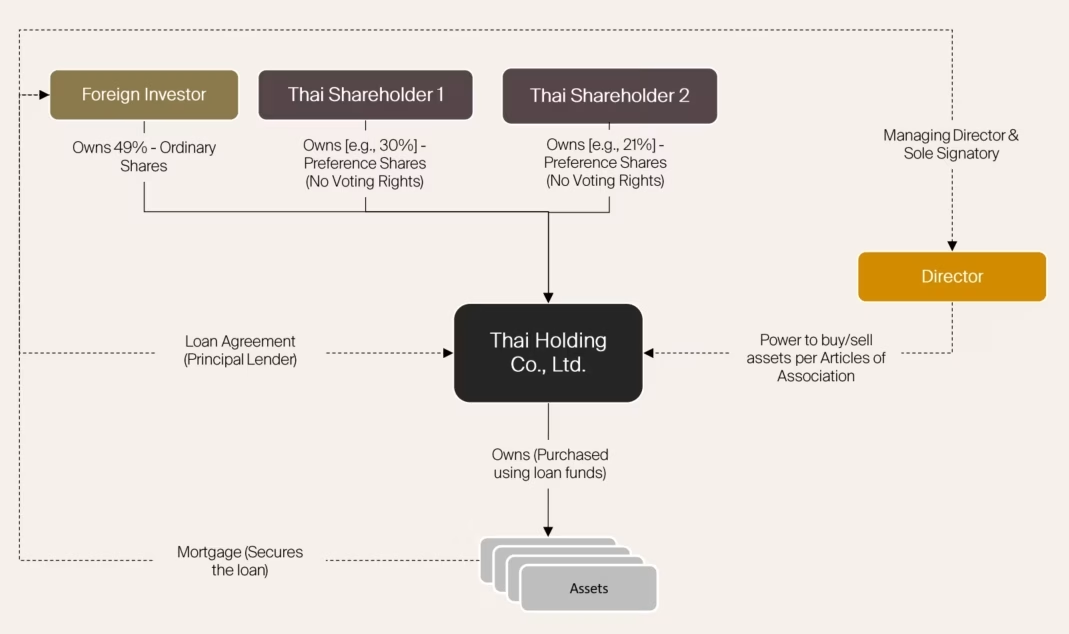

The Thai Company Structure (Holding Structure)

The company structure rests on three pillars that work in unison to give the foreigner effective control despite holding only 49% of shares:

- Absolute Directorial Authority: The foreigner is appointed as sole Managing Director. The Articles of Association grant this role exclusive power to buy, sell, lease, and mortgage all company assets without board or shareholder approval.

- Engineered Share Structure: The foreigner's 49% are Ordinary Shares (with voting rights). The Thai nationals' 51% are Preference Shares (no voting rights on critical decisions, only entitled to a fixed dividend).

- Secured Financial Leverage: The foreigner provides funds as a formal personal loan to the company, secured by a mortgage registered in their personal name over the property. This provides an enforceable fallback.

The LTR Visa: The Property Investor's Ace Card

For anyone planning to buy property worth 250,000 USD or more, the Long-Term Resident (LTR) Visa is the strategic move that simultaneously solves your residency and investment goals.

Why the LTR Visa Changes Everything

Pro Tip: If you plan to buy a condo worth over $250,000 USD (approx. 8–9 million THB), apply for the LTR Visa using that purchase as your qualifying investment. It simultaneously secures your home and a 10-year residency permit in one move.

Key Financial Benchmarks

2026 Cost of Living by City

Bangkok: The Urban Metropolis

Living in Bangkok means world-class dining, a thriving bar scene, elite shopping, and the best private hospitals in Southeast Asia. This convenience carries the highest price tag in Thailand.

| Lifestyle | Monthly Budget (USD) | What It Gets You |

|---|---|---|

| Comfortable Expat | ~$2,200 / 80,000 THB | 1BR condo near BTS, mix of local/Western food, Grab transport, good health insurance, solid entertainment budget. |

| Luxury Living | ~$4,100+ / 150,000+ THB | Premium 2BR condo (Sukhumvit), frequent fine dining, private driver or own car, premium healthcare coverage. |

Chiang Mai: The Relaxed North

Consistently ranked the #1 expat destination in Southeast Asia. Laid-back atmosphere, proximity to nature, and significantly lower costs than Bangkok.

| Lifestyle | Monthly Budget (USD) | What It Gets You |

|---|---|---|

| Frugal & Local | ~$950 / 35,000 THB | Nice studio condo, eating primarily local food, scooter for transport, basic insurance. A very happy, achievable lifestyle. |

| Comfortable Expat | ~$1,500 / 55,000 THB | Modern 1–2BR condo in Nimman, frequent café dining, good health insurance, budget for travel and hobbies. |

Pattaya: The Beachside Playground

More expensive than Chiang Mai, more affordable than central Bangkok. A vibrant coastal lifestyle with good infrastructure for retirees.

| Lifestyle | Monthly Budget (USD) | What It Gets You |

|---|---|---|

| Comfortable Expat | ~$1,800 / 65,000 THB | Modern 1BR sea-view condo, local and international dining mix, Baht bus / Grab transport, solid entertainment budget. |

| Luxury Living | ~$3,300+ / 120,000+ THB | Spacious condo in premium building or private pool villa, frequent fine dining, own car. |

How Long Will Your Savings Last?

If you prefer to think in terms of spending down a fixed amount without investing, this table shows approximately how long a lump sum will last. These calculations do not account for inflation — in practice your savings will run out faster as costs rise.

| Your Total Savings | Years at $1,500/month | Years at $2,000/month | Years at $2,500/month |

|---|---|---|---|

| $100,000 USD | ~5.5 years | ~4.2 years | ~3.3 years |

| $300,000 USD | ~16.6 years | ~12.5 years | ~10 years |

| $500,000 USD | ~27.7 years | ~20.8 years | ~16.6 years |

| $750,000 USD | ~41.6 years | ~31.2 years | ~25 years |

The 4% rule states that you can withdraw 4% of your invested nest egg annually with a high probability of it lasting 30+ years. At a $2,000/month spending target, your required annual income is $24,000 — meaning you need a $600,000 USD invested nest egg to retire sustainably. An uninvested savings account would require significantly more capital.

Debunking the "Early Retirement" Myth

Every Muay Thai gym and nomad café has someone in their early 30s who claims to be "retired" in Thailand. The reality is almost always one of four scenarios:

| The Story | The Reality |

|---|---|

| The "Digital Nomad Retiree" | The most common group. Not retired — working remotely. Flexible hours create the appearance of retirement, but they have active income streams. |

| The "Sabbatical Taker" | Living off savings accumulated at home for 1–3 years. This is a temporary lifestyle, not a permanent retirement. The money eventually runs out. |

| The Beneficiary | Receiving family wealth, inheritance, or a trust. Their passive income is not something they earned but rather received. |

| The FIRE Achiever | The rarest group. Worked high-paying roles, lived frugally for 10–15 years, and built a $1M+ invested nest egg through extreme discipline. |

Visa & Tax Requirements for Retirees

Retirement Visa (Non-Immigrant O-A / O-X)

Thailand Elite / LTR Visa (Premium Path)

The 2026 Tax Reality

As of 2026, the 2024 Revenue Department ruling is in full enforcement. If you spend 180 days or more in Thailand in a calendar year, you are a Thai tax resident. This means:

- Remittance Basis: You are only taxed on foreign income (dividends, pensions, interest) that you bring into Thailand. Funds that remain offshore are generally not taxed.

- Pre-2024 Savings Exemption: Funds earned before January 1, 2024 are generally exempt if you can document their origin. This is a key strategy for anyone migrating significant capital.

- Double Taxation Treaties: Most retirees from the US, UK, and Australia are protected from double taxation on government pensions. However, administrative filing is now often required even if you owe zero Thai tax.

- TIN Requirement: Thai banks and immigration are increasingly requesting Tax Identification Numbers (TINs) to maintain foreign accounts. Build an accounting fee (~$300/year) into your miscellaneous budget to engage a local tax professional.

Financial Tools & Apps

📱 Airalo eSIM

Activate a Thai data SIM before you land — no SIM queue, no airport kiosk tourist tax. Essential for receiving the TrueMoney registration OTP the moment you clear immigration.

Get Your eSIM »💳 Wise

Send money from your home currency to a Thai bank account at mid-market rates. Also excellent as a stop-gap debit card if set up in your home country before departure.

Visit Wise »🏨 Agoda

In Southeast Asia, Agoda consistently beats Booking.com on rates and inventory for long-stay condos, serviced apartments, and monthly rental deals.

Find Deals »✈️ Trip.com Flights

Book fully refundable onward flights to satisfy Thai Immigration's "proof of onward travel" requirement at the border — and avoid being denied boarding.

Book Refundable Flights »📈 Interactive Brokers (IBKR)

The gold standard for non-US expats investing in Thailand. Direct SET access, multi-currency accounts including THB, and accepted from 200+ countries.

Visit IBKR »🔄 Revolut

The best card for daily spending in Thailand — mid-market exchange rate, zero foreign transaction fees. Open and receive the card at home before departure.

Visit Revolut »Official Government & Regulatory Sources

📋 Bookmark These Official Links

Your Financial Edge, Activated

Thailand's financial system is not designed to make life easy for foreigners. The ATM fees, DCC traps, bank account barriers, and complex property laws are real. But none of them are insurmountable. Armed with this playbook, you now know exactly which card to use at the checkout, which bank to target with which strategy, which investment structures are legal and which carry risk, and what you actually need saved before you can call this place home. The numbers are clear. The tools exist. The only question is whether you use them.

Chrome → ⋮ → Print → Paper: A4 · Margins: None · ✅ Background graphics